Revenue

$44.5bn

'21-'26 5.2 %

'26-'31 1.0 %

Enter your work email to explore our industry research on the IBISWorld platform.

Australia Industries by SectorAustralia Products

Australia Industries by SectorAustralia Products

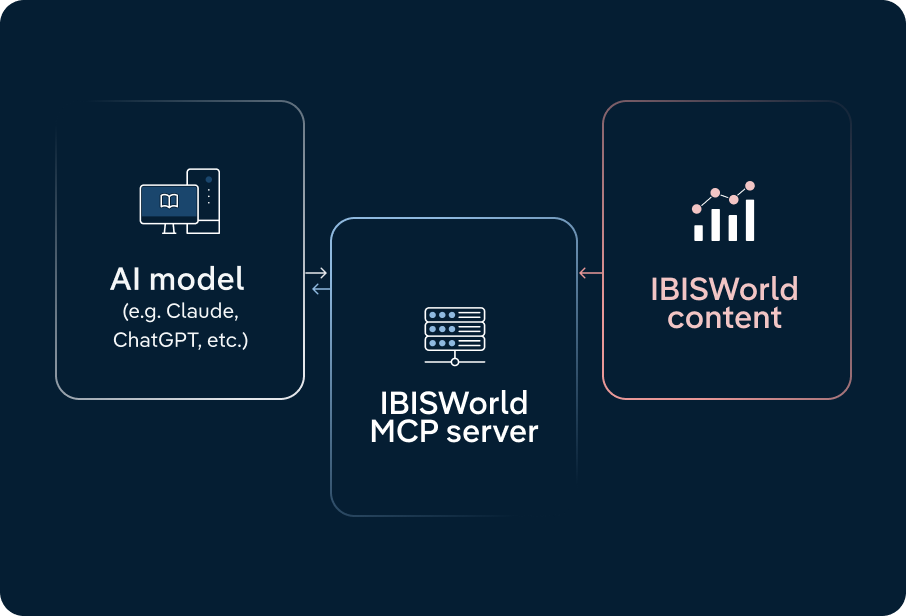

Pull large datasets straight from the IBISWorld database.

Build company datasets across financials, segments, and benchmarks.

Connect IBISWorld data directly to your workflows.

Learn more about MCP US 11111

US 11111

Farms in this industry grow soybeans as their main crop. Soybeans are most often used in livestock feeds and vegetable oils, with a small but growing proportion used in biofuel production. Establishments that sell soybean seeds to US farmers for growing crops are also included.

Surging biofuel demand and record domestic crush are creating new opportunities for soybean farmers, but overall revenue remains under pressure after several years of weak prices and heavy global supplies. Many growers are responding by shifting acres toward soy and pushing for higher yields and better basis near crush and biofuel hubs to support profit in a still-challenging price environment.

Climate change will add volatility to crop yields and force farmers to reassess production practices. The effects of extreme seasons and weather events will likely inhibit production, supporting prices, though farmers will also face higher operating costs.

US soybean exports are under pressure as Brazil ramps up production and China cuts its US imports. Farmers are diversifying markets to sustain their trade volume, emphasizing quality and sustainability to stay competitive.

Go to chapterRefineries need soybean oil for biodiesel. Biofuel production has grown after supply chain disruptions at home and abroad increased gas and diesel prices during the current period.

Health consciousness among buyers is a challenge to soybeans in the edible oil market. Consumers are spending a premium on oils they see as healthier and avoiding seed oils.

Go to chapter| Key External Drivers | Impact |

|---|---|

| Demand from organic basic chemical manufacturing | Positive |

| World price of soybeans | Positive |

| Trade-weighted index | Negative |

| Subsidies for soybean farming | Positive |

| Characteristic | Level | Trend |

|---|---|---|

| Concentration | Low | |

| Barriers To Entry | High | Steady |

| Regulation and Policy | Moderate | Steady |

| Life Cycle | Growth | |

| Revenue Volatility | High | |

| Assistance | Moderate | Steady |

| Competition | Moderate | Increasing |

| Innovation | Low |

Industry revenue for soybean farmers in the US has contracted over the past five years, even as structural demand from domestic crushers and biofuel producers has strengthened the underlying market. Industry revenue has fallen at a CAGR of 5.2% since 2021 to an estimated $44.5 billion in 2026, including a 1.9% decline in 2026. Robust growth in soybean oil use for biomass-based diesel and renewable diesel, combined with record or near-record crush volumes, has helped offset weak export demand and provided a floor under prices, but not enough to fully counteract the revenue drag from the earlier price downturn and rising operating expenses. New and expanded crush capacity has supported local basis improvements around processing and biofuel hubs, giving nearby growers a relative price advantage and incentivizing acreage shifts toward soy, yet overall industry performance remains constrained by high fertilizer, fuel and labor costs and the lingering impact of 2024/25's multi-year price lows.

Trade and export markets remain a central swing factor for the industry, with recent volatility reshaping both current performance and the medium-term outlook. China's pullback from US soybeans during 2025 tariff tensions, and its ongoing pivot toward Brazilian supplies, have sharply reduced US export volumes to China, eroding one of the industry's highest-value outlets even as domestic crush expanded. A new framework announced in late 2025, under which China committed to purchase at least 25 million metric tons of US soybeans annually through 2028, has stabilized flows and supported prices but still leaves exports below pre-trade-war peaks and subject to policy risk. Looking ahead, USDA long-term projections suggest US export volume growth will be modest and more diversified, with incremental gains in Latin America, North Africa, the Middle East and Southeast Asia partially offsetting structurally lower dependence on China.

Over the next five years, industry revenue is forecast to continue contracting, shrinking at a CAGR of 1.1% to $42.4 billion in 2031 as modest volume gains and firm demand fail to fully overcome persistent price and cost headwinds. Soybean and soybean oil prices are projected to improve into the 2026/27 season on the back of record biofuel mandates, tighter balance sheets and record crush, but then soften over the remainder of the outlook period, limiting topline growth even as demand for oil and meal remains solid. At the same time, climate-related yield pressures, higher input requirements and regional production risks will keep operating costs elevated, constraining profitability despite gradual export recovery and continued domestic demand growth. As a result, the industry's outlook is characterized less by a strong cyclical rebound and more by a slow, policy-driven stabilization in which efficient, well-located producers near crush and biofuel hubs are best positioned to outperform in an otherwise unfavorable revenue environment.

Refineries need soybean oil for biodiesel. Biofuel production has grown after supply chain disruptions at home and abroad increased gas and diesel prices during the current period.

Health consciousness among buyers is a challenge to soybeans in the edible oil market. Consumers are spending a premium on oils they see as healthier and avoiding seed oils.

By investing in R&D, soy farmers can improve crop yields, enhance disease resistance and reduce environmental impacts, which helps maintain competitiveness and address the evolving demands of the agricultural sector.

Accessing high-quality seeds and nutrients ensures optimal plant growth and productivity. This helps soy farmers to produce higher yields and meet market quality standards, ultimately contributing to business success.

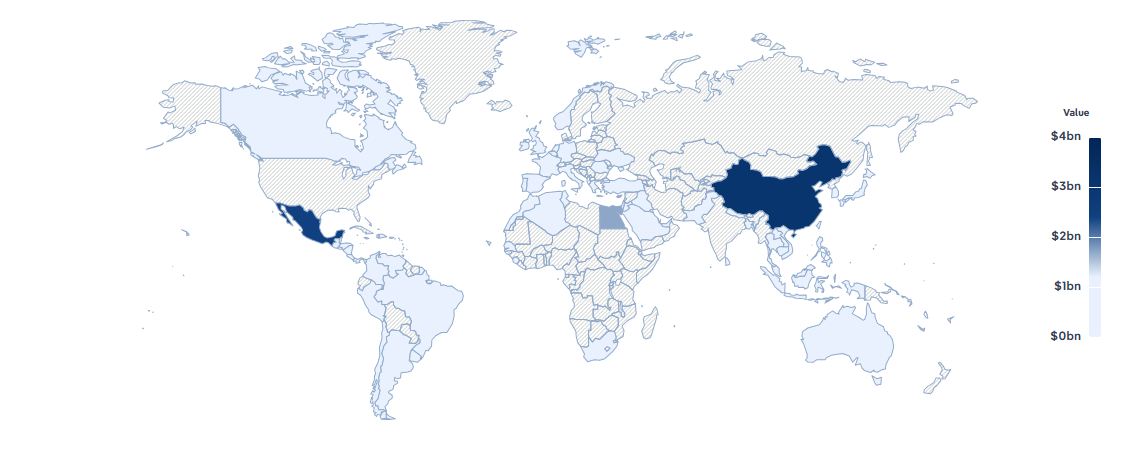

Exports account for more than half of US soybean sales, making the industry highly trade-exposed, while imports are negligible. A depreciating US dollar and diversification beyond China toward Latin America, North Africa, the Middle East and Southeast Asia are expected to support a gradual export recovery over the outlook period.

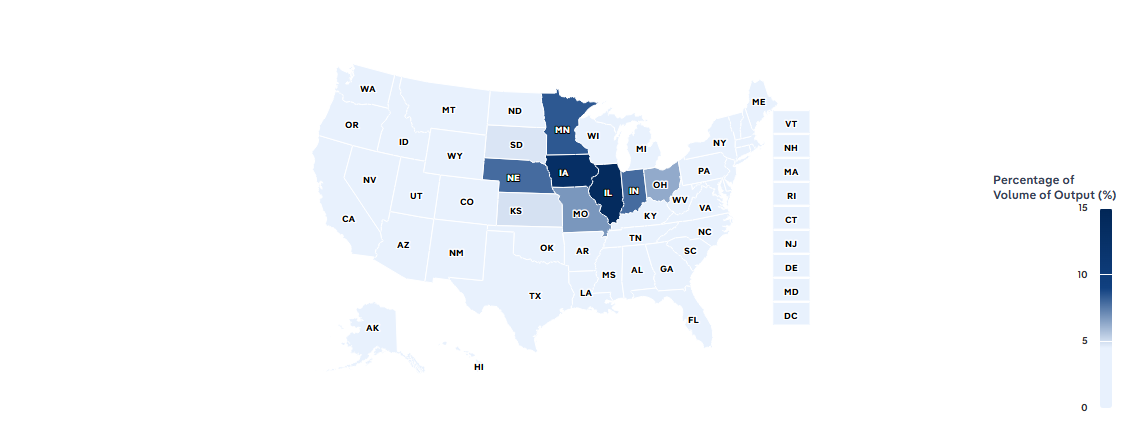

Soybean plants need large fields of open space. The Plains region grows nearly half of the US soybeans because, in addition to climate, it has the necessary acreage dedicated to farmland.

The Great Lakes limit their region's drought potential. Consistent supplies of water and irrigation make the lakes' surrounding states ideal for stable soybean growing.

| State | Volume of Output (Units) | Population % |

|---|

New technology has enabled soybeans to be raised in areas that were previously too difficult to cultivate. However, yields may be insufficient to justify planting and harvesting costs; careful assessment is needed to determine the best choice for planting location and quantity.

Soybean farms can benefit from operating in areas with longer growing seasons or conditions that allow for crop rotation and off-season production.

Soybean farms will need to aggressively lower per-bushel costs through scale, efficiency gains and precision input use to stay competitive with other soybean, feed grain and oilseed producers. While some farms can differentiate through identity-preserved, non-GMO or sustainability-certified beans, the industry remains highly price-sensitive, so the lowest-cost producers will capture the most demand over the next few years.

Health-focused alternatives have created a threat to soybeans in both the edible oil and animal feed markets. Some consumers have turned away from soybean and other seed oils due to concerns around the extraction process and high levels of omega-6 fatty acids.

Soybean farms need a steady supply of seeds, so having a set contract with a seed producer can limit volatility risk and help keep production volumes stable.

Many small, family-owned soybean farms have limited resources and can benefit from membership in an industry organization that promotes resource sharing.

Achieving economies of scale allows US soybean farmers to lower production costs by maximizing output. This cost efficiency provides a competitive edge, enabling them to navigate market volatility and enhance profitability, which is crucial for overcoming barriers to entry.

Securing supply contracts provides a stable and reliable source of essential farming inputs. This stability helps mitigate risks associated with fluctuating input prices, enabling new entrants to maintain consistent production and better manage cash flow.

Producing a differentiated product allows US soy farmers to offer unique attributes such as non-GMO or organic soy, appealing to niche markets and consumer preferences. This differentiation reduces the threat from substitute crops and enhances market competitiveness.

Gaining in-depth technical knowledge about soy cultivation enables farmers to optimize crop yields and adapt to environmental changes. This expertise helps maintain high-quality standards, ensuring soy's competitiveness and reducing the appeal of alternative crops in the market.

Accessing international buyers diversifies revenue streams and reduces dependence on domestic markets, helping soybean farmers dilute individual buyer influence and manage concentrated buyer power more effectively.

Competitive pricing attracts more buyers and strengthens farmers' market position, improving their ability to negotiate contracts, manage basis risk and partially offset concentrated buyer power.

Soybeans are grown in the US almost exclusively by small companies. While some companies produce seeds on a large scale, nearly all soybean farms are small, independent operations. The volatile and labor-intensive nature of soybean farming makes it difficult for one company to capture significant market share.

| Company | Market Share (%) | Employees | Locations | Company Type | Headquarters |

|---|---|---|---|---|---|

| Carroll Family Farms | 2.5-5 | 5,001-10,000 | 2 | Private | Carthage, Illinois |

| Baker Farms | 0-2.5 | 51-200 | 1 | Private | Columbus, Georgia |

| Saginaw Valley Seedcorn | 0-2.5 | 51-200 | 1 | Private | Fairgrove, Michigan |

Discover deeper company data with IBISWorld's Atlas tool.Go to Atlas

Discover deeper company data with IBISWorld's Atlas tool.Go to Atlas Government subsidies help protect soybean farmers when soybean prices decline. Subsidies also reduce risk from revenue volatility caused by harsh growing conditions and adverse weather.

A depreciating US dollar will support a recovering export market. Exports already account for more than half of soybean sales. As the dollar depreciates, exports will grow further.

Demand from organic chemical manufacturing boosts the soybean industry since soybeans serve as a raw material for biodegradable plastics, lubricants and other plant-based products. As industries and consumers increasingly prioritize sustainable products, soybean derivatives see rising demand, providing farmers with additional revenue streams.

The world price of soybeans directly affects farmers' profitability and planting decisions. High global prices incentivize increased production; low prices strain revenues and reduce innovation. Price fluctuations also influence export competitiveness. A drop in soybean prices poses a threat to the industry.

The trade-weighted index, which reflects the value of the US dollar against other currencies, substantially impacts soybean exports. A strong dollar makes US soybeans more expensive abroad, reducing demand and export revenue. Conversely, a weaker dollar enhances competitiveness, boosting exports since US soybeans become cheaper for international buyers. This economic measure guides strategic export decisions and influences international market share and industry growth. Any depreciation in the US dollar presents an opportunity for US soybean farmers.

Government subsidies provide financial stability for soybean farmers in the form of a buffer against market volatility and adverse weather, which can otherwise threaten farm income and credit access. These bolsters help producers maintain operations, invest in productivity-enhancing technologies and adopt sustainable practices that improve long-term soil and resource management. By increase security and thereby reducing financial risk, subsidies stabilize soybean supply chains, support consistent national production levels and strengthen overall sector resilience.

The Clean Water Act regulates discharges of pollutants into US and affects soybean farming primarily through limits on water pollution. Agricultural stormwater runoff and return flows from irrigated agriculture are generally exempt from federal NPDES permitting when they result from precipitation or normal irrigation, although discharges that involve dredged or fill material into jurisdictional waters can still require authorization. As a result, soybean farmers are not usually required to obtain federal discharge permits for ordinary runoff, but they are still expected to implement best management practices, such as buffer strips near streams, cover crops, reduced tillage and careful fertilizer timing, to minimize sediment, nutrient and pesticide losses to nearby waters and to avoid activities in wetlands or streams that would trigger permitting.

FIFRA governs the registration, sale and use of pesticides in the United States, including those applied to soybeans. Before pesticides can be marketed, the EPA evaluates and registers them, sets use restrictions and establishes label directions intended to manage risks to human health and the environment. For soybean farmers, compliance largely means using only registered products and strictly following the pesticide label, which has the force of federal law, for application rates, timing, methods, buffer requirements, personal protective equipment and drift restrictions, as well as adhering to storage, disposal and record-keeping practices that many labels and state laws require.

The Federal Seed Act is a federal truth-in-labeling law that regulates the interstate shipment of agricultural and vegetable seed, including soybean seed. It requires that seed containers carry accurate information on seed kind and, where applicable, variety, as well as quality characteristics such as purity percentage, germination rate, the presence of noxious weed seeds and any chemical seed treatments. For soybean producers, this framework helps ensure that purchased seed lots meet advertised standards and the labels disclose key attributes, such as genetic variety, quality and treatments, so farmers can make informed planting and stewardship decisions.

The Renewable Fuel Standard requires that specified volumes of renewable fuels, including biomass-based diesel and other advanced biofuels made from soybean oil, be blended into the US fuel supply. The EPA's "Set" rules for 2023 through 2025 and the follow-on 2026 through 2027 standards have established increasing volume targets for biomass-based diesel and total renewable fuel, underpinned by expectations of continued growth in biofuel use. This regulatory framework has significantly expanded industrial use of soybean oil for biofuel relative to traditional food markets and, based on USDA and EPA projections, is expected to keep upward pressure on soybean oil demand and influence planting and crushing decisions over the next several years.

Conservation compliance provisions under the Food Security Act link eligibility for many federal farm program benefits to the protection of highly erodible land and wetlands. Soybean farmers who produce crops on highly erodible land without an approved conservation plan, or who drain or convert wetlands to enable crop production, risk losing access to these benefits until they correct the violation or obtain relief, so in practice they must maintain conservation plans, avoid new wetland conversions and implement erosion-control practices to remain eligible.

The EPA's Agricultural Worker Protection Standard is a federal regulation designed to reduce the risks of pesticide exposure for workers and handlers on farms, including soybean operations. Soybean farmers who employ workers to mix, load or apply pesticides – or to enter treated fields – must provide safety training and access to decontamination supplies, post treated-area warnings and observe restricted-entry intervals listed on pesticide labels. The WPS also requires recordkeeping and emergency response information so that employees can obtain medical care promptly if exposure occurs, which affects how soybean farms schedule spraying and organize labor during the growing season.

The USDA's Farm Service Agency (FSA) and Natural Resources Conservation Service (NRCS) provide financial assistance, technical support and conservation planning that directly affect soybean producers' cost structure and risk profile. FSA administers commodity, disaster and loan programs; NRCS helps soybean farmers design and implement conservation practices like nutrient management, cover crops and erosion control on working cropland. For example, soy producers commonly work with a local NRCS office to develop a conservation plan, and then use FSA to establish a farm number and access payment and loan programs tied to that plan. This coordinated framework supports both farm income stability and compliance with conservation and eligibility requirements specific to field-crop operations like soybeans.

The Federal Crop Insurance Program, run by the USDA's Risk Management Agency, offers subsidized yield and revenue insurance that covers most planted soybean acres in the US. Soybean farmers can choose from Yield Protection or Revenue Protection; in practice, the federal government subsidizes a substantial share of the premium and shares underwriting risk with private insurers. This coverage helps producers insure against losses from drought, excess moisture, disease and price declines, helping them secure operating credit and withstand bad crop years.

The Environmental Quality Incentives Program, administered by the Natural Resources Conservation Service, provides cost-share and technical assistance for conservation practices on working lands like soybean fields. Soybean growers can receive multiyear contracts to help pay for practices – such as cover crops, reduced tillage, nutrient management and on-farm drainage or water-quality improvements – and NRCS typically shares a significant portion of installation costs. In recent years, EQIP has supported expanded cover-crop adoption in row-crop systems. For soybean producers, this assistance can reduce erosion, improve soil structure and meet sustainability expectations from downstream buyers while offsetting up-front practice costs.

Programs like the Export Credit Guarantee Program's GSM-102 (Guaranteed Sales Mechanism) provide credit guarantees to encourage financing of commercial exports of US agricultural products, including soybeans. By reducing financial risk to lenders, these guarantees support sales to buyers in primarily developing countries that have the foreign exchange capacity to meet scheduled payments. Under authority provided in recent farm legislation, the USDA regularly allocates substantial annual guarantee capacity to back export credit for eligible commodities. USDA has kept GSM-102 active and has expanded and refined its export-financing options over time to boost global demand for US farm products, reinforcing its ongoing relevance for soybean exports.

The ASA helps soybean farmers by advocating for favorable policies, securing research funding and promoting sustainable farming practices. By representing farmers' interests in legislative discussions, the ASA helps shape trade policies that enhance market access and competitiveness. It also provides farmers with resources, educational programs and support networks to navigate the market and adopt new innovation. The ASA seeks to ensure that soybean farmers have the tools and support needed to manage a dynamic agricultural environment.

Cooperatives support soybean farmers by pooling resources to help farmers can reduce costs, increase profitability and gain better access to markets. This enables farmers to purchase inputs at lower prices and sell their products in larger markets for better rates. Cooperatives also offer benefits like legal support and the potential for improved product quality, contributing to rural development. For instance, they often provide shared facilities like storage and processing plants, helping smaller farmers access economies of scale.

The United Soybean Board manages the national Soy Checkoff program, investing mandatory farmer assessments in research, promotion and education to build demand and resilience for US soybeans. The USB approved budgets of $174 million dollars for 2025 and $121 million dollars for 2026, targeting areas like infrastructure, animal nutrition, bio-based product development and export promotion, which helps soybean farmers tap new markets and meet evolving sustainability expectations without having to coordinate these efforts individually.

Input costs remain elevated for soybean farms, with fertilizer, fuel and labor still materially higher than pre-2021 levels even after retreating from their peaks at the start of the current period. Farmers who were unable to lock in inputs before the latest energy-driven price spikes are facing tighter profit on average than better-capitalized operations that secured lower-cost supplies.

Profit for soybean farmers has fluctuated alongside soybean prices. The volatility of these price changes has made it difficult for farmers to quickly balance their costs with falling prices.

| Year | Revenue per Employee ($) | Revenue per Enterprise ($M) | Employees per Estab. | Employees per Enterprise | Average Wage ($) | Wages/Revenue (%) | Estab. per Enterprise | IVA/Revenue (%) | Imports/Demand (%) | Exports/Revenue (%) |

|---|

| Year | Revenue ($M) | IVA ($M) | Estab. (Units) | Enterprises (Units) | Employment (Units) | Exports ($M) | Imports ($M) | Wages ($M) |

|---|

Download the entire report.

Our generative AI-powered economist designed to streamline your research.

Industry revenue for soybean farmers in the US has contracted over the past five years, even as structural demand from domestic crushers and biofuel producers has strengthened the underlying market. Industry revenue has fallen at a CAGR of 5.2% since 2021 to an estimated $44.5 billion in 2026, including a 1.9% decline in 2026. Robust growth in soybean oil use for biomass-based diesel and renewable diesel, combined with record or near-record crush volumes, has helped offset weak export demand and provided a floor under prices, but not enough to fully counteract the revenue drag from the earlier price downturn and rising operating expenses. New and expanded crush capacity has supported local basis improvements around processing and biofuel hubs, giving nearby growers a relative price advantage and incentivizing acreage shifts toward soy, yet overall industry performance remains constrained by high fertilizer, fuel and labor costs and the lingering impact of 2024/25's multi-year price lows.

Trade and export markets remain a central swing factor for the industry, with recent volatility reshaping both current performance and the medium-term outlook. China's pullback from US soybeans during 2025 tariff tensions, and its ongoing pivot toward Brazilian supplies, have sharply reduced US export volumes to China, eroding one of the industry's highest-value outlets even as domestic crush expanded. A new framework announced in late 2025, under which China committed to purchase at least 25 million metric tons of US soybeans annually through 2028, has stabilized flows and supported prices but still leaves exports below pre-trade-war peaks and subject to policy risk. Looking ahead, USDA long-term projections suggest US export volume growth will be modest and more diversified, with incremental gains in Latin America, North Africa, the Middle East and Southeast Asia partially offsetting structurally lower dependence on China.

Over the next five years, industry revenue is forecast to continue contracting, shrinking at a CAGR of 1.1% to $42.4 billion in 2031 as modest volume gains and firm demand fail to fully overcome persistent price and cost headwinds. Soybean and soybean oil prices are projected to improve into the 2026/27 season on the back of record biofuel mandates, tighter balance sheets and record crush, but then soften over the remainder of the outlook period, limiting topline growth even as demand for oil and meal remains solid. At the same time, climate-related yield pressures, higher input requirements and regional production risks will keep operating costs elevated, constraining profitability despite gradual export recovery and continued domestic demand growth. As a result, the industry's outlook is characterized less by a strong cyclical rebound and more by a slow, policy-driven stabilization in which efficient, well-located producers near crush and biofuel hubs are best positioned to outperform in an otherwise unfavorable revenue environment.

Surging biofuel demand and record domestic crush are creating new opportunities for soybean farmers, but overall revenue remains under pressure after several years of weak prices and heavy global supplies. Many growers are responding by shifting acres toward soy and pushing for higher yields and better basis near crush and biofuel hubs to support profit in a still-challenging price environment.

Climate change will add volatility to crop yields and force farmers to reassess production practices. The effects of extreme seasons and weather events will likely inhibit production, supporting prices, though farmers will also face higher operating costs.

US soybean exports are under pressure as Brazil ramps up production and China cuts its US imports. Farmers are diversifying markets to sustain their trade volume, emphasizing quality and sustainability to stay competitive.

With exports making up a considerable share of the soybean market, entering into contracts insulates companies against the risk of price fluctuations.

Government assistance payments can improve farmer income in good and bad harvest years. See the Industry Assistance section for details regarding specific programs.

Despite its maturity, the soybean farming industry in the US has seen a declining contribution to GDP in recent years due largely to its strong volatility and crop price drops that have reversed the industry growth seen early in the current period.

The market for soybean farming in the US is largely saturated, but there remains room for growth, particularly in niche markets like organic soybeans and climate-resistant varieties, as well as soy-based plastics. Outside of these markets, however, soy is well-entrenched as a staple food product and biofuel input. Farmers can grow their market by looking outside of these traditional use cases and partnering with innovative processors to explore new possibilities.

Innovation in US soybean farming is focused on incremental change, with the development of products such as GMOs, organic variants and climate-resistant seeds. These advancements can open new markets and provide more high-value product offerings. Government funding supporting the development of sustainable agriculture techniques and producing organic products has bolstered innovation in these segments.

Consolidation in the soybean farming industry has been low and consistent, characterized by gradual acquisitions and partnerships rather than aggressive mergers. This steady consolidation reflects a stable competitive landscape, allowing farmers to optimize operations and manage resources effectively without drastic industry changes.

The integration of advanced technology and systems, such as precision agriculture and data-driven decision-making tools, has been focused on improving existing soybean farming operations. These technologies increase efficiency, optimize resource use and reduce environmental footprints, boosting productivity and ensuring the sustainability of soybean cultivation.