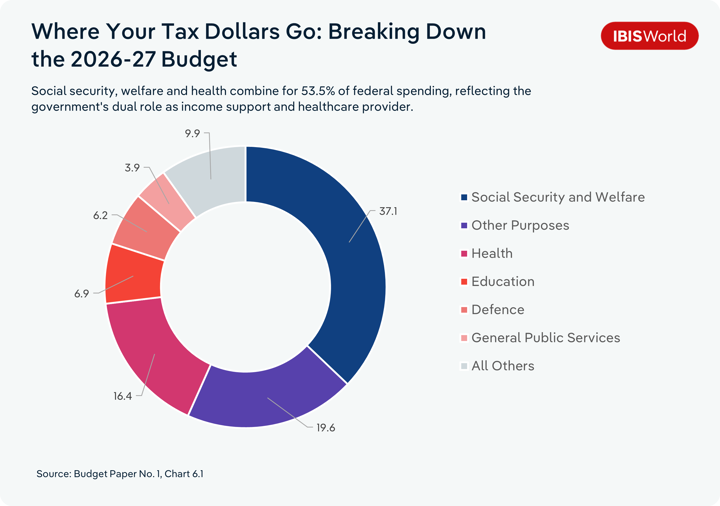

Key Takeaways

- Housing reform aims to improve affordability and redirect investment towards new dwelling construction, though weaker investor demand may pressure short-term residential building activity.

- Manufacturing, construction materials and defence supply chain industries are positioned to benefit from productivity-focused reform, compliance cost reductions and rising investment in fuel security.

- Persistent inflation, elevated borrowing costs and global energy market volatility continue to pose significant risks for households, businesses and the broader economic outlook.

Jim Chalmers delivered his fifth consecutive Federal Budget for the Australian Labor Party on 12 May 2026. It marks only the second time since 2000 that a government has handed down five consecutive budgets, highlighting the sustained challenge of balancing economic growth and fiscal discipline while maintaining social cohesion and funding essential services.

State of Affairs

The 2025 Federal Budget served as the launching pad for the Labor Party’s re-election campaign. As households grappled with elevated living costs, the government focused on delivering immediate relief while largely avoiding politically divisive tax reform debates. Key measures included income tax cuts, energy bill rebates, HECS/HELP debt relief and expanded Medicare funding, all aimed at easing pressure on household budgets while reinforcing the government’s cost-of-living credentials ahead of the election.

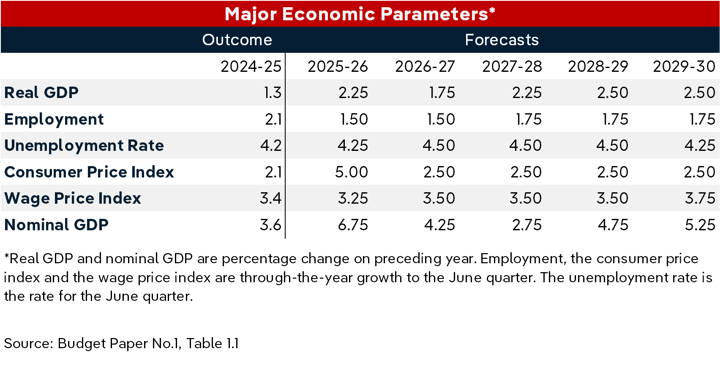

The 2026 Federal Budget arrives under similarly difficult, and in some respects more challenging, economic conditions. Unlike last year, the government now has the political advantage of a fresh electoral mandate and several years before Australians return to the polls, providing greater scope for structural reform. Economic conditions have deteriorated in recent months, with the Reserve Bank lifting interest rates three times since the beginning of 2026 in response to renewed inflationary pressures in the second half of 2025. Escalating and prolonged tensions in the Middle East have also heightened concerns around global energy markets and fuel security, contributing to higher transport and energy costs and strengthening the RBA’s hawkish stance. As a result, expectations surrounding the 2026 Budget have again centred on cost-of-living relief, housing affordability and fiscal sustainability, while also addressing mounting concerns over inflation, energy security and rising national debt.

National Debt

The decisions outlined in the Federal Budget carry significant implications for Australia’s broader economic position and long-term fiscal sustainability. According to the latest Government Finance Statistics released by the Australian Bureau of Statistics, Australia’s general government net debt reached $982 billion in 2025-26, equivalent to 33.1% of GDP. Debt levels have remained above 30.0% of GDP since 2019-20, reflecting the substantial borrowing undertaken during the pandemic and the years that followed.

The new Budget is expected to increase debt levels by $211.0 billion in nominal terms over three years, where it will peak at 35.8% of GDP in 2028-29. While the government argues this is below the debt trajectory inherited from the previous government in 2022, the spending is likely to place significant pressure on future governments to make difficult fiscal consolidation decisions, effectively deferring the hard choices needed to return to structural budget balance.

Housing and Construction

The Budget’s capital gains tax (CGT) discount reforms and removal of negative gearing represent some of the most significant housing policy reforms under consideration as the government attempts to address worsening housing affordability.

The proposed reforms are expected to reduce investor tax advantages, potentially easing competition for first-home buyers. The changes are anticipated to commence from July 2027 and will primarily apply to newly built dwellings to avoid a sharp sell-off of existing investment properties while continuing to encourage new housing supply.

Treasury has previously referenced analysis from the Grattan Institute and the Centre for Independent Studies indicating that limiting negative gearing and reducing the CGT discount could lower housing prices by an estimated 1.0% to 4.0%, potentially improving affordability for first-home buyers.

Even so, the construction sector could face weaker demand conditions if reduced investor incentives and an extension of the foreign investor ban until 2029 shrink the pool of prospective buyers. Industry groups have argued that implementing the reforms during an already subdued construction cycle could place additional pressure on house construction activity, an industry that was beaten down by the high cost of borrowing over the three years through 2024-25. With dwelling commencements already forecast to soften, reduced investor participation may delay recovery across the construction sector, particularly in investor-heavy multi-unit apartment and townhouse construction markets.

Exemptions or concessions tied to newly built dwellings may partially redirect investor demand towards new housing stock, supporting greenfield residential development. Land development and subdivision operators may experience stronger demand as buyers seek vacant residential lots and newly developed land to build homes that qualify for the proposed tax concessions.

To support housing activity, the Federal Government has proposed a $2.0 billion Local Infrastructure Fund to finance the roads, water and utility connections required to unlock new housing developments. Heavy and civil engineering construction, road and bridge construction and construction machinery and operator hire providers are set to benefit from this increased spending on roads, pipelines, drainage and electricity connections. Smaller engineering contractors and heavy construction firms may also experience stronger project pipelines as councils accelerate enabling infrastructure.

Defence

Defence spending is set to rise to 3.0% of GDP by 2033 under NATO measurement standards, with the Federal Government committing an additional $53.0 billion over the next decade as Australia seeks to strengthen its defence capabilities amid escalating geopolitical tensions.

Despite the sizeable headline figure, the investment profile suggests limited near-term economic stimulus. Much of the funding incorporates previously announced projects, including the estimated $12.0 billion upgrade of the Henderson Shipyard in Western Australia. Budget projections indicate that only around $14.0 billion of the additional spending will occur before 2030, with expenditure heavily back-ended into the later years of the forecast period, including $8.7 billion in 2033-34 and $9.8 billion in 2034-35.

The government has also flagged between $2.0 billion and $5.0 billion to invest in drone and autonomous warfare capabilities, driving demand for aircraft manufacturing and repair services. However, the inclusion of existing projects within the broader funding envelope raises questions over how much of the spending represents genuinely new economic activity rather than repackaging or expanding on existing commitments.

Maritime defence programs account for a substantial share of the investment pipeline. Alongside upgrade to the Henderson and Osborne, SA, shipyards, the Budget includes between $4.8 billion and $5.8 billion over the decade for autonomous and uncrewed sea warfare systems, providing significant demand for shipbuilding and repair services. Western Australia and South Australia are well positioned to capture much of the economic benefit from shipbuilding, defence infrastructure and advanced manufacturing. While many large platform contracts have already been awarded, significant portions of the broader supply chain remain open to tender, potentially creating opportunities for small and mid-size manufacturers and engineering firms located within these manufacturing hubs.

Manufacturing

The Budget included limited direct spending for manufacturing, with much of the sector’s support flowing indirectly through investment in fuel security, defence and infrastructure. Instead, the government’s primary manufacturing reform centred on reducing regulatory and compliance costs, targeting an estimated $10.2 billion in annual savings across businesses as it attempts to address long-standing productivity challenges.

Construction-related manufacturing industries are positioned to benefit most from the reforms. Free access to Australian Standards will remove a significant compliance cost for building product manufacturers and construction material producers, builders and tradies. Streamlined planning and approval processes may also accelerate construction timelines, supporting stronger demand for a range of manufacturers, including those producing fabricated metal products, plaster products, concrete products and carpentry and joinery timber.

Food manufacturing may also benefit from lower compliance costs and the permanent extension of the $20,000 instant asset write-off, which is expected to encourage smaller operators to invest in processing equipment, automation and productivity-enhancing technology. Meat processing is one industry that has increasingly adopted automation to reduce wage costs and improve competitiveness against low-cost overseas producers, with the expanded asset write-off expected to support this transition.

Energy and Fuel

The Budget’s most significant energy-related initiative was the more than $14.8 billion Australian Fuel Security and Resilience package, aimed at expanding strategic fuel reserves and strengthening domestic fuel supply capabilities amid heightened geopolitical tensions and oil market volatility.

Petroleum product wholesalers, petroleum refiners and petroleum fuel manufacturers and bulk fuel storage operators gain access to government-backed financing to expand storage capacity and inventory levels from the current 27 to 30 days’ worth of supply to 50 days for diesel and aviation fuel.

The package is designed to protect fuel-reliant industries like freight transport, aviation, mining, construction and manufacturing from severe price spikes and supply shortages. By improving energy security, the government is attempting to give businesses greater confidence to continue investing and operating despite ongoing geopolitical uncertainty.

The Budget also included measures aimed at strengthening fertiliser security, reflecting Australia’s reliance on imported fertiliser products. Increased domestic capabilities and more data storage support are intended to reduce future price volatility and improve supply reliability for farmers. The measures are expected to provide agricultural producers like grain growers and vegetable growers with greater confidence to maintain production, invest in cropping programs and make longer-term capital decisions.

The Federal Government is set to gradually wind back fringe benefits tax (FBT) concessions for electric vehicles (EVs) purchased through novated leasing arrangements. Under the proposed changes, EVs valued above $75,000 will attract partial FBT liabilities from April 2027, while concessional treatment for all EVs is expected to be reduced from 2029.

The reform places motor vehicle wholesalers in a difficult position. Reduced tax incentives may weaken consumer demand for EVs, yet the New Vehicle Efficiency Standard is simultaneously pressuring wholesalers and manufacturers to increase EV imports to avoid penalties tied to high-emission vehicle sales. Electric vehicle wholesalers will hope recent events highlighting Australia’s vulnerability to global fuel shocks, which have helped drive stronger EV demand, don’t lose momentum following the reduction in tax incentives.

Health

The largest health-related measure in the Budget was the government’s decision to slow projected growth in the National Disability Insurance Scheme (NDIS) – generating an estimated $15 billion in savings over four years – alongside major increases in Medicare and hospital funding. The Budget included a renewed National Health Reform Agreement, representing an additional $25 billion in funding beyond existing commitments, alongside $1.8 billion over five years to make Medicare Urgent Care Clinics permanent.

Allied health services and other health care services linked to Medicare-funded primary care are expected to benefit from increased public healthcare spending and measures to improve affordability and accessibility. Urgent care clinics, general practice medical services and pharmaceutical providers may experience stronger patient volumes as bulk billing incentives and public health access expand. Private hospitals could also benefit indirectly if expanded public funding reduces pressure on emergency departments and improves referral pathways.

However, disability support providers heavily exposed to the NDIS may face slower revenue growth and tighter compliance requirements as eligibility rules tighten.

Private health insurers may experience modest support if pressure on the public health system encourages higher-income households to retain cover, although changes to private health rebates for older Australians could weaken participation among retirees.

Inflation Outlook

Inflation remains one of the defining economic risks shaping the 2026-27 Federal Budget. While many of the government’s measures are aimed at easing pressure on households through targeted relief and infrastructure investment, elevated public spending risks adding to demand at a time when inflationary pressures remain persistent.

The RBA has already set the stage for a hawkish 2026 following renewed inflation concerns. Continued fiscal spending and ongoing energy market volatility risk slowing the disinflation process.

For industry, sustained inflation and higher borrowing costs are expected to prolong margin pressure across fuel-intensive sectors. Freight transport operators, manufacturers, construction firms and airlines may continue facing elevated fuel and financing costs, while retailers could experience weaker discretionary spending as households remain cautious.

Final Word

The 2026-27 Federal Budget reflects an economy under pressure from persistent inflation, elevated living costs and growing geopolitical uncertainty. Rather than relying on large-scale short-term stimulus, the government has focused on structural reform, aiming to balance household relief with longer-term measures to improve housing affordability, boost productivity and strengthen economic resilience.

Housing reforms are expected to reshape investment patterns across residential property markets, pushing investors to support future construction activity. Manufacturing policy has centred less on direct subsidies and more on improving productivity through compliance reform and investment incentives, while healthcare providers are still positioned to benefit from rising public spending despite broader fiscal restraint.

Ultimately, the Budget paints a picture of a government attempting to navigate an increasingly difficult economic environment. While inflation is forecast to moderate over time, global fuel volatility, slowing economic growth and elevated borrowing costs are likely to continue weighing on households and businesses. The Budget’s success will largely depend on whether its structural reforms can generate long-term investment and productivity growth without reigniting inflationary pressure.